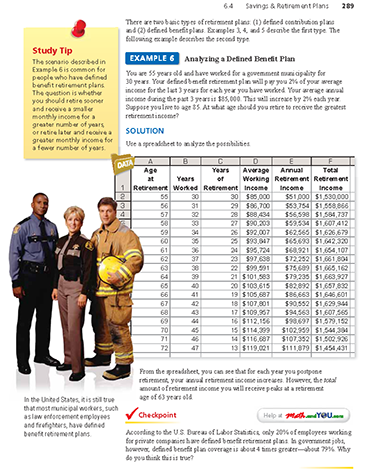

-

There are many assumptions used to create the spreadsheet in Example 6. One important assumption is how long you can expect to live. According to data compiled by the Social Security Administration (SSA):

- A man reaching age 65 today can expect to live, on average, until age 83.

- A woman turning age 65 today can expect to live, on average, until age 85.

Also, about one out of every four 65-year-olds today will live past age 90, and one out of 10 will live past age 95. You can use the SSA's life expectancy calculator to estimate how long you might live. You can also estimate your Social Security benefits. To estimate how much you need to save to fund your retirement, make a spreadsheet or try using an online calculator.

-

Have you ever wondered what job will get you the best retirement benefits? You might be surprised to learn that jobs in the utilities industry typically pay out the best retirement benefits, with an average of $4.22 per hour.

For a list of which jobs will earn you the most money for retirement, check out this article in U.S. News & World Report.

-

Sample answer:

Defined contribution plans are subject to market risk. A defined contribution plan with investments that do poorly will negatively affect a person's retirement income. A defined benefit plan, on the other hand, pays the same amount to the retiree no matter what. If the market doesn't do well, the employer, who still has to pay the promised amount, will be the only one hurt. This risk is the reason many companies have defined contribution plans instead. The government has much more money to work with than the average company and people will always be paying taxes, so market risk isn't as big of a problem. For this reason, government jobs are much more likely to have defined benefit plans than private sector jobs.

-

Comments (1)

These comments are not screened before publication. Constructive debate about the information on this page is welcome, but personal attacks are not. Please do not post comments that are commercial in nature or that violate copyright. Comments that we regard as obscene, defamatory, or intended to incite violence will be removed. If you find a comment offensive, you may flag it.

When posting a comment, you agree to our Terms of Use.Showing 1 commentsSubscribe by email Subscribe by RSS Ron Larson (author)1 decade ago |The problem in Example 6 is called an optimization problem. In this case, you are trying to optimize the total retirement income you will receive. Remember, however, that optimizing your total retirement income is only one part of the decision. By retiring earlier, you will get less, but you will have more years (at a younger age) to enjoy retirement.0 0

Ron Larson (author)1 decade ago |The problem in Example 6 is called an optimization problem. In this case, you are trying to optimize the total retirement income you will receive. Remember, however, that optimizing your total retirement income is only one part of the decision. By retiring earlier, you will get less, but you will have more years (at a younger age) to enjoy retirement.0 0