-

A spreadsheet was used in Example 3 to make an amortization table. This is a useful method for homeowners who are trying to keep up with their mortgage balance, as well as their home's equity.

To access a home's equity, a homeowner can obtain a second mortgage. A second mortgage is a loan that uses the home as collateral to guarantee repayment and allows the homeowner to receive the full amount at once and to repay it over a fixed period of time. A homeowner can also obtain a home equity line of credit (HELOC). A HELOC is a loan that uses the home as collateral to guarantee repayment and is structured as a revolving line of credit, similar to a credit card: the lender agrees to lend a maximum amount of money within an agreed period of time, and the borrower can use the entire credit line, or borrow specific amounts from time to time. The interest rate on a HELOC is generally variable, although some lenders offer fixed rate HELOCs. For more information, read "What you should know about home equity lines of credit."

-

You can drastically reduce the life of your mortgage loan and amount paid in interest by increasing your principal payments. To see the changes that would occur for a specific loan, check out E-Loan for a mortgage amortization calculator.

-

-

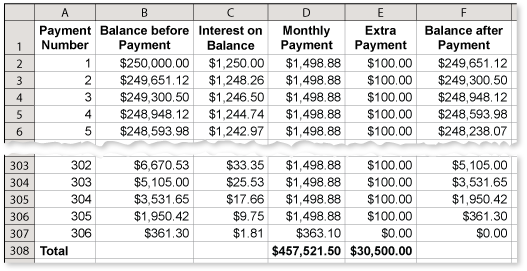

An amortization schedule showing the effect of the additional $100 monthly payment is shown in the spreadsheet.

You pay off the mortgage after 306 months, which is 4.5 years sooner.

-

By making the additional payments, you paid a total of

This is a savings of

-

-

Comments (1)

These comments are not screened before publication. Constructive debate about the information on this page is welcome, but personal attacks are not. Please do not post comments that are commercial in nature or that violate copyright. Comments that we regard as obscene, defamatory, or intended to incite violence will be removed. If you find a comment offensive, you may flag it.

When posting a comment, you agree to our Terms of Use.Showing 1 commentsSubscribe by email Subscribe by RSS Ron Larson (author)1 decade ago |Example 3 is a great example. One way to think of a principal payment is that once you have paid the interest on your mortgage for a month, you are generally free to pay any additional amount directly to the principal. It is surprising that additional payments of even $10 or $25 can end up saving you thousands of dollars in interest.0 0

Ron Larson (author)1 decade ago |Example 3 is a great example. One way to think of a principal payment is that once you have paid the interest on your mortgage for a month, you are generally free to pay any additional amount directly to the principal. It is surprising that additional payments of even $10 or $25 can end up saving you thousands of dollars in interest.0 0