-

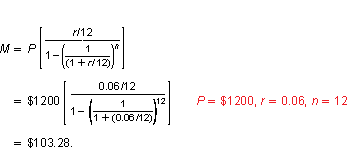

There are several ways that you can calculate the monthly payment for an installment loan or to create an amortization table.

- by hand

- using a calculator

- using a spreadsheet (see Example 1)

- using an online calculator (Note that a Monthly Payment Calculator is located in Tools.)

Depending on which method you use, your numbers may differ by a few pennies from what is shown in the examples and answers. This may occur due to how the figures are rounded. Be sure you understand the concepts described in this section and do not get distracted by numbers that differ by only a few pennies.

It should be noted that when computing monthly payments and amortization schedules, some lending institutions round to the nearest cent. Other institutions give themselves a slight advantage by always rounding up to the next highest cent when calculating interest due to them. In most transactions, the total difference in these two rounding procedures should amount to only a few pennies.

Sometimes, the final payment will need to be adjusted due to round-off error in calculating the monthly payment. To find the final payment in an amortization schedule, add the balance before the final payment to the final interest payment.

-

The next time you need to take out a loan for a major purchase you might want to check out Bankrate.com, which can help you find out what lender has the best interest rates in your area.

-

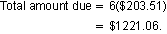

The loan proceeds are $1200 and the total amount due is

So, the cost of credit is

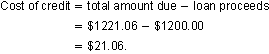

If the loan term doubles, the monthly payment becomes

The cost of credit for this loan is

No, the cost of credit does not double when the loan term doubles. The relationship between cost of credit and term is more complicated than that. As term increases, cost of credit may increase at a slower or faster rate depending on the interest rate and the initial term length.

-

Comments (2)

These comments are not screened before publication. Constructive debate about the information on this page is welcome, but personal attacks are not. Please do not post comments that are commercial in nature or that violate copyright. Comments that we regard as obscene, defamatory, or intended to incite violence will be removed. If you find a comment offensive, you may flag it.

When posting a comment, you agree to our Terms of Use.Showing 2 commentsSubscribe by email Subscribe by RSS Guest 3 years ago |Although the formula resembles a building floor plan, it is greatly helpful.1 0

Guest 3 years ago |Although the formula resembles a building floor plan, it is greatly helpful.1 0 Ron Larson (author)1 decade ago |In the table in Example 1, you can see the general pattern for amortization tables. As the balance of your loan decreases, the amount of your monthly payment that goes toward interest decreases.1 0

Ron Larson (author)1 decade ago |In the table in Example 1, you can see the general pattern for amortization tables. As the balance of your loan decreases, the amount of your monthly payment that goes toward interest decreases.1 0